Robo-advising is an awesome new development in the investing world. Robo-advisors can manage funds autonomously and automatically rebalance portfolios to desired allocations depending on performance. Robo-advising and robo-investing have significantly lowered the bar for getting into the investment world.

As such, several robo-advising firms have popped up in the past few years, Wealthify is one of these services. Wealthify is a robo-advising firm that leverages a team of expert advice and modern algorithms to create custom portfolios.

We are always interested in robo-advising platforms that aim to push the envelope. In this article, we cover Wealthify and answer some key questions you might have about the platform. We will cover the pros, cons, features, and fees. At the end, we will give our verdict on whether Wealthify is worth it or not.

What Is Wealthify?

Wealthify is a UK-based robo-advising service that was launched relatively recently back in 2017. They have followed a popular trend among robo-advisors, specialising in managing exchange-traded funds (ETFs) as its main investment asset class. In a nutshell, Wealthify uses sophisticated economic models to passively manage client funds in a way that minimises risk and maximises return.

Wealthify has been through a bit of a rollercoaster journey in its ~5 years in existence. Wealthify was bought by Aviva after years of significant growth and has expanded its original offering. As of June 2020, Wealthify is a wholly-owned subsidiary of Aviva.

Wealthify is created by a group of “like-minded investment experts, software engineers, and entrepreneurs” who want to cause waves in the investing world while making investing affordable and accessible to everyone.

How Does Wealthify Work?

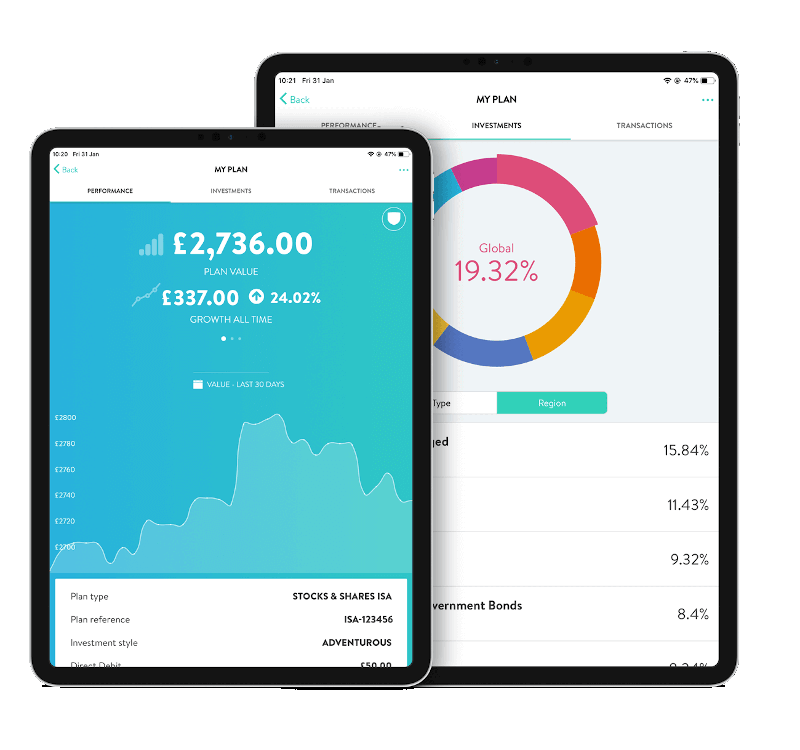

Wealthify works like many investment services. You create an account, select your investments, then watch as your wealth starts to grow. Wealthify’s key distinguishing feature is that it employs a team of experts to analyse client funds. This team of experts analyses decisions according to economic algorithms to keep portfolio allocations in line with customer preferences. Wealthify has both a desktop site and a mobile app.

Anyone 18 or older living in England, Scotland, Wales, or Northern Ireland can sign up for a GIA account. Unfortunately, US citizens cannot open a Wealthify account due to banking and tax reporting regulations. When you apply, you will be asked for some financial info like your bank details and credit references for identity checks. Wealthify does NOT run a credit check and the application process will not negatively affect your credit.

Once you sign up, you can choose the kind of account you want to create. Wealthify currently supports:

- General investment accounts (GIA)

- Individual Savings Accounts (ISA)

- Junior ISA (JISA)

- Pensions (SIPPs)

None of Wealthify’s accounts have a minimum deposit, except for SIPPS which have a minimum £50 account balance. More details on that here.

Along with the three accounts, you will be prompted to select if you want ‘ethical’ investing for your accounts. Ethical investing plans will screen selections from so-called ‘sin-stock’ (stock from alcohol, gambling, tobacco, etc.) and identify stock from companies that utilize sustainable and socially responsible practices.

Once you select an account type, you will be asked some questions to determine your risk tolerance. Then you will be prompted to choose your allocation selections. Wealthify offers 5 portfolio structures to choose from:

- Cautious

- Tentative

- Confident

- Ambitious

- Adventurous

The Cautious option dumps the majority of your funds into government and corporate bonds. Only about 12% of your funds will be in shares, property, and currencies.

The confident setting is a good middle-of-the-road selection that has a well-balanced structure. The confident plan spreads your assets more equally among UK/foreign shares and US/UK/EU corporate and government bonds. A little less than 50% of your assets will be held in foreign currencies under this allocation.

Lastly, the Adventurous plan puts most of your funds into European and American shares, with some in Japanese and Asian markets. This plan has the riskiest allocation of assets but consequently has the highest potential yield. Additionally, each portfolio structure has an ‘ethical’ option which mimics the same allocations but with the appropriately screened stocks.

All in all, the whole signup process takes just a few minutes. The signup process is actually much less frustrating than a lot of other investment services.

There is one kind of weird quirk we noticed though: When you sign up, you are asked a bunch of questions about your risk tolerance; things like: “How would you feel if your investments fell in a 12 month period?” or “What is your current savings level?”

Depending on how you answer, you can actually be rejected from Wealthify; for example, if you have no savings and a lot of debt. It’s pretty cool that they added this courtesy feature in case investing is really not a good idea for you. Looks like that’s the company abiding by their moral and fiduciary duties. You can always go back and change your answers though, so you can still invest with Wealthify no matter what.

What Fees Does Wealthify Charge?

Wealthify makes the majority of its revenue through management fees. Up until 2019, Wealthify used to have different rates for accounts with different deposit amounts. But back in December 2019, they changed things to a standard flat 0.6% fee across all account types. At low account balances (<£100k) this is lower than a lot of other UK robo-advising firms like Nutmeg and Moneyfarm. But several other firms have lower rates for accounts with £100K+ deposited.

Aside from management charges, Wealthify has a 0.22% fund charge for their ETFs, which is pretty standard across the industry. Aside from the management fee and the fund fees, Wealthify does not charge anything else. There are no minimum account penalties and there are no fees for when your portfolio is rebalanced.

Is Wealthify Legit? Is My Money Safe?

Yes, Wealthify is a legitimate organization and your money will be securely deposited with them. Wealthify works through companies that are regulated by the Financial Conduct Authority which means that your funds could not be targeted by creditors. Also, up to £85,000 of your investments are backed by the Financial Services Compensation Scheme.

Wealthify uses two custodians to hold customer assets. Winterflood Securities Limited holds the funds to GIA and ISAs while Embark Investment Services Limited holds the funds for pensions.

As always, FSCS coverage does not protect you if your investments perform poorly and you lose money. However, you should not really have to worry about that. Based on data from the past 3 years, Wealthify has managed to perform as well as other robo-advising firms for moderately risky investments. To be clear, this data is only for 3 years so this trend might not hold in the future.

What Else Does Wealthify Do?

Aside from robo-advising-related services such as rebalancing, Wealthify does not do anything else. Wealthify is not an advisory service so they are not regulated to provide advice to investors. Strictly speaking, the term ‘robo-advisor’ is a bit of a misnomer as robo-advisors don’t actually advise anyone. They just automate the investment process.

If you feel like you need a quick refresher on the ins-and-outs of robo advisors, check out our guide here.

Wealthify Benefits

Simplified approach: The best part of Wealthify (and this is true for robo-advisors in general) is the simplified approach. It is very easy to make an account, deposit funds, and watch your wealth grow with little to no effort on your part. A lot of people don’t invest because it seems too complex and they are intimidated. Services like Wealthify do wonders for bringing investing to a wider audience.

Good portfolio selection: Wealthify offers 5 pre-tailored portfolios, which is actually more than a lot of other providers. Although you can’t select your individual allocations, the 5 plans cover a good range of risk/reward. Plus, the option for ethical investing is a good draw for socially conscious investors.

Low fees: Wealthify has relatively low management fees, compared to other investment services at only 0.6%. However, this fee applies to all accounts, regardless of the amount invested.

Wealthify Drawbacks

No advising: Wealthify is purely a robo-advisor. They do not offer human advisory services. O unfortunately, you can’t talk to someone at the company to figure out your investing goals.

Limited reach: Wealthify only operates in the UK and can only accept UK citizens. For us Brits, that’s perfect but for anyone else, sorry that you are out of the loop.

Flat fee: Wealthify’s fee is low for accounts under £20,000. But it is higher than a lot of services that offer reduced fees for high-value accounts.

Our Verdict: Is Wealthify Worth It?

Yes, Wealthify is worth it. The best part of robo-advising services like Wealthify is that it makes things so simple and intuitive. There are no minimum account balances so even if you just have £50 lying around you can get started investing. Wealthify offers a decent spread of investment selections and portfolio allocations.

If you are looking for more direct hands-on control with investing, then Wealthify may not be the best fit for you. However, if you are looking for passively managed funds, then it’s a good choice.

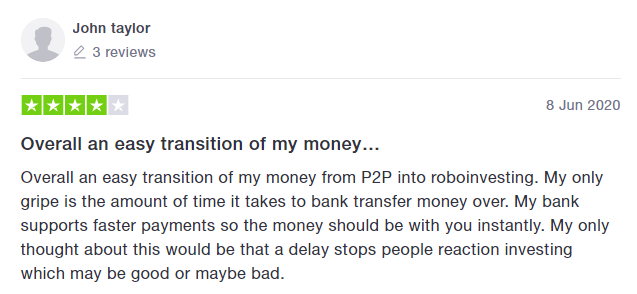

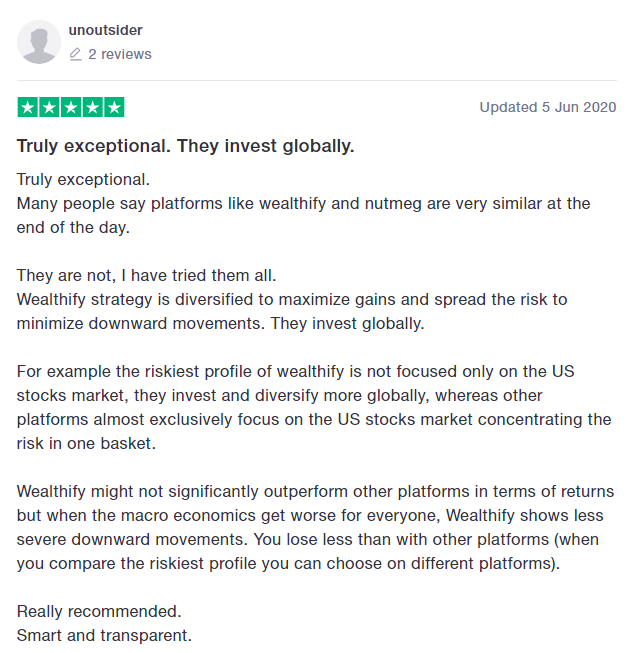

What Are Other People Saying About Wealthify?

- The 9 Best UK Money Management Apps (2025) – for individuals and couples - August 8, 2024

- What Salary Should You Be Making At Your Age? (UK Guide) - August 8, 2024

- The Top 10 Most Ethical Banks in the UK: A Comprehensive Review for 2025 - August 8, 2024