There is a whole wide world out there for things to spend your money on. Millennials may know this more than anyone. Although it can be used as more of a buzzword than a defined group of people, the truth is, the word “millennial” is often synonymous with being “irresponsible”.

What may surprise you, however, is that millennials do manage to save some of their money from time to to time. In this article, we’ll define who a millennial is, showcase what they are saving for, and detail some of the best habits and trends for millennials interested in saving money.

Who exactly are Millennials?

Okay, so let’s define exactly who a Millennial is. According to Wikipedia, “millennial” is a label that can be used to describe a person from the generation born between roughly 1981 and 1996. Millennials are often also called Generation Y or simply Gen Y, because they fall along the timeline between Generation X and Generation Z.

Millennials get their nickname from having lived through the new millennium (year 2000) at an early age. Some born slightly after 2000 may adopt the millennial moniker as well. And of course, occasionally a “cool” member of an older generation will adopt a new technology in order to declare themselves an “honorary” millennial.

Are Millennials Good at Saving?

Despite what many people might think, yes, millennials are good at saving money.

According to a Chase Bank Generational Money Talks Study, millennials begin saving money for retirement at age 23. Compared to ages 30 and 40 for Gen X and Baby Boomers respectively, millennials are getting a head start on putting money away for themselves.

With that being said, no millennial is perfect, no matter how many Instagram followers they have.

According to a survey from the American Institute of Certified Public Accountants, impulse buying is still holding many millennials back from achieving their financial goals.

What Are Millennials Saving For?

However you slice it, one of the most consistent narratives with the millennial generation is a devaluation in material goods. Millennials are known for wanting “experiences” rather than expensive possessions.

Many analysts believe that millennials cannot even imagine saving enough money for a house due to university debt, increased cost of living, and lower wages. However, the generation has lived through enough economic crises to take financial stability seriously.

In the same survey mentioned above, millennials say they are most like to save money for:

- An Emergency Fund

- Large Purchases (Car, house, home improvements)

- Retirement

- Starting a Family

- A Wedding

So clearly, survival is a millennial’s number one priority. With an emergency fund in line and large necessities purchased, a small percentage of millennials can begin thinking about saving extra money for retirement, starting a family, or a dream wedding.

Analysing The Stats

How Much Do Most Millennials Have in Savings?

This is where it gets ugly. The hard truth is that, in the UK, over half of millennials between the ages of 22 and 30 have absolutely no savings whatsoever.

Although the young adults are less likely to be in debt from a large purchase, it is fairly disturbing to see how little financial security most millennials have. Those who did save, had a reported average of £1,600 stowed away.

How Much are Millennials Saving Each Month?

Of course, the most common way to get started saving money is by putting a small amount of it away once or twice per month. Although there is a large variance in investment level, 84% of millennials do put some money away in savings each month. On average, millennials have around £176 per month, which is around £7.50 less than the national average.

How Do Millennials Save Money?

So clearly, some millennials are saving money, but perhaps more should consider adjusting their lifestyle in order to do so.

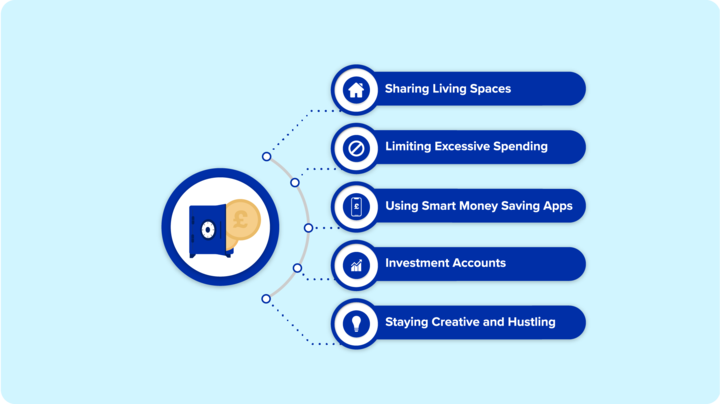

Here are five of the best habits and trends that millennials are using to help lower expenses and increase their wealth.

1. Sharing Living Spaces

Flatmates can be a bit much sometimes, especially if they are your parents. About 1 in 4 young adults in the UK are still living at home. Although this may not be perfect for your social life, it is actually a great way to cut down on monthly expenses.

Increasing rent prices make living alone less affordable year after year. For those without the luxury of a family home, renting a flat with multiple tenants can also drive down monthly costs. So even though adding a flatmate to an already small area can crowd your personal space, your wallet will also become crowded with all that extra money you save.

For millennials, finding paying tenants has never been easier. With social media, online communities, and listing sites like Airbnb, it is very possible to find someone looking to rent every kind of living space.

2. Limiting Excessive Spending

Impulse buying is perhaps millennials greatest weakness. Dream vacations and expensive plates of sushi are sometimes too hard to pass up in the eyes of someone with a little extra money lying around.

Of course, it is also important to treat yourself to the things in life that you enjoy. However, there are a few habits that are popular amongst millennials in decreasing overall, unnecessary spending. These include:

- Limitations on eating out at restaurants

- Packing a lunch for work

- Brewing Coffee at Home (Sorry, Starbucks)

- Buying Items that are on sale

- Lowering monthly subscription services (for television, music, home goods, etc.)

Essentially, every bit of your income that you don’t spend on something that you don’t truly need in order to live can become a part of your savings. Don’t go crazy however, remember to live a little!

3. Using Smart Money Saving Apps

As millennials like to say, “there’s an app for it.” Sometimes saving money can be as easy using your smartphone. In the UK, there are many apps designed to help you save money for whatever it is you are financing. Some are free of service, while others charge a fee.

A savings app will generally work in one of two ways. For many, the apps have an interface in which you can set up a recurring deposit of a small amount of money daily, weekly, bi-weekly or monthly. In these apps, it is easy to set a goal and arrange a schedule to finance it on your own terms.

Secondly, there are a few apps that help you save various amounts of money based on your spending habits. Not so long ago, people had large jars to put spare change in at the end of the day. Today, we have virtual “round-up” services that will add a little bit of money to your savings account every time you purchase something.

4. Investment Accounts

Remember the old phrase, “it takes money to make money?” While this is not always true, it certainly is in the case of an investment account. Traditionally, UK residents save up for retirement by paying into a pension or an ISA. Whereas this is still commonplace with some millennials, as you can imagine, new digital options are also emerging.

Just like apps for saving money, there are many apps for investing money available in the UK. There are a lot to choose from, each with their own algorithms, operating modes, fees, and more. Some of our favourites that we’ve reviewed in the past include:

With new technologies being developed every day, this is only a small snapshot of the many investment apps available today.

5. Staying Creative and Hustling

Lastly, millennials are generally not shy to “disrupt” or attempt to completely change the way things are traditionally done. As the younger generation transitions into full-blown adulthood, more and more millennials are finding creative ways to both earn and save more money.

There are many ways to shave a few pounds here and there on normal spending. This includes:

- Student Perks

- Loyalty Discounts

- Customer Referrals and Rebates

- Side Businesses

- Renting Out Assets

Essentially, saving money can be as time consuming as you would like. Keeping an eye out for new ways to save money or earn a little extra income can help pave the way for better financial health.

Conclusion

Overall, millennials are simply finding ways to get by, just as any other generation. Although they may not own as much property, smart saving habits and technologies have enabled many millennials to begin saving years before previous generations. Financial security can lead to an overall better life, so we hope that this article has been helpful in exploring today’s top millennial saving habits and trends.

- The 9 Best UK Money Management Apps (2025) – for individuals and couples - August 8, 2024

- What Salary Should You Be Making At Your Age? (UK Guide) - August 8, 2024

- The Top 10 Most Ethical Banks in the UK: A Comprehensive Review for 2025 - August 8, 2024